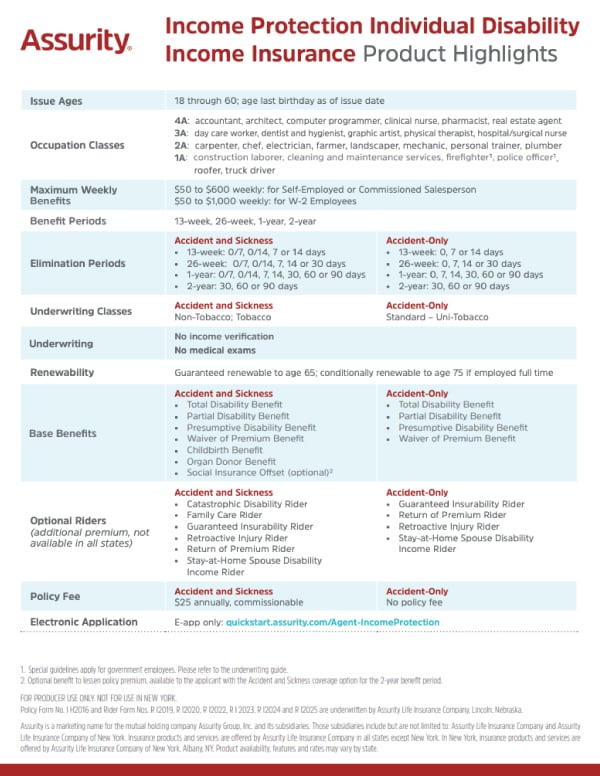

Highlight Sheet

Seller's Guide

On-demand Training

Sales Ideas

Class 6A

![]() ~1.6M jobs

~1.6M jobs

![]() $81,680 median income3

$81,680 median income3

With high participation in employer retirement plans and stable earnings, many accountants need protection during long-duration earning years.

Class 6A

![]() ~865K jobs

~865K jobs

![]() $151,160 median income3

$151,160 median income3

Attorneys are looking to protect high lifetime earnings, with considerations for residual coverage tied to billable capacity.

Class 4A

![]() ~1.5M jobs

~1.5M jobs

![]() $104,900 median income3

$104,900 median income3

Strong but variable income and exposure to physical risk or business dependency make it critical to design coverage that fits the real work being performed.

Class 4A

![]() ~3.4M jobs

~3.4M jobs

![]() $93,600 median income3

$93,600 median income3

This fast-growing workforce faces repetitive physical demands – supplement employer benefits to create lasting protection.

Class 5A

![]() ~532K jobs

~532K jobs

![]() $56,320 median income3

$56,320 median income3

Drive sales by protecting against residual disability costs in this market with commission-based income and variable earnings.

Class 5A

![]() ~1.54M jobs

~1.54M jobs

![]() $62,340 median income3

$62,340 median income3

Stable employment and strong employer benefits; place more business by designing protection that coordinates with existing coverage.

Class 3A

![]() ~222K jobs

~222K jobs

![]() $94,260 median income3

$94,260 median income3

Dental hygienists face partial disabilities due to repetitive fine motor tasks – create coverage that can suit part-time work or jobs in multiple offices.

Class 2A

![]() ~2.2M jobs

~2.2M jobs

![]() $57,440 median income3

$57,440 median income3

Customize coverage to offer affordable protection in a large market with higher exposure to risks.

Class 6A

![]() ~4.4M jobs

~4.4M jobs

![]() $132,903 median income3

$132,903 median income3

Fill gaps in employer coverage to create opportunities in this high-income market with long earning horizons.

Accountant (CPA)

Class 6A

![]() ≈1.6M jobs

≈1.6M jobs

![]() $81,680 median income3

$81,680 median income3

With high participation in employer retirement plans and stable earnings, many accountants need protection during long-duration earning years.

Attorney

Class 6A

![]() ≈865K jobs

≈865K jobs

![]() $151,160 median income3

$151,160 median income3

Attorneys are looking to protect high lifetime earnings, with considerations for residual coverage tied to billable capacity.

Dental Hygienist

Class 3A

![]() ≈222K jobs

≈222K jobs

![]() $94,260 median income3

$94,260 median income3

Dental hygienists face partial disabilities due to repetitive fine motor tasks – create coverage that can suit part-time work or jobs in multiple offices.

General Contractor

Class 6A

![]() ≈1.5M jobs

≈1.5M jobs

![]() $104,900 median income3

$104,900 median income3

Strong but variable income and exposure to physical risk or business dependency make it critical to design coverage that fits the real work being performed.

Real Estate Agent

Class 5A

![]() ≈532K jobs

≈532K jobs

![]() $56,320 median income3

$56,320 median income3

Drive sales by protecting against residual disability costs in this market with commission-based income and variable earnings.

Registered Nurse

Class 4A

![]() ≈3.4M jobs

≈3.4M jobs

![]() $93,600 median income3

$93,600 median income3

This fast-growing workforce faces repetitive physical demands – supplement employer benefits to create lasting protection.

Sales Representative

Class 4A/5A

![]() ≈1.3M jobs

≈1.3M jobs

![]() $80,490 median income3

$80,490 median income3

Sales representatives rely on commission and variable income – build a strong story around partial disability and protecting production.

Software Developer

Class 6A

![]() ≈4.4M jobs

≈4.4M jobs

![]() $132,903 median income3

$132,903 median income3

Fill gaps in employer coverage to create opportunities in this high-income market with long earning horizons.

Teacher

Class 5A

![]() ≈1.54M jobs

≈1.54M jobs

![]() $62,340 median income3

$62,340 median income3

Stable employment and strong employer benefits; place more business by designing protection that coordinates with existing coverage.

Traveling Nurse

Class 4A

![]() ≈175K jobs

≈175K jobs

![]() $109,512 median income3

$109,512 median income3

Strong earnings and inconsistent benefits create a strong need for portable protection and residual disability coverage.

Truck Driver

Class 2A

![]() ≈2.2M jobs

≈2.2M jobs

![]() $57,440 median income3

$57,440 median income3

Customize coverage to offer affordable protection in a large market with higher exposure to risks.

Software Developer

Class 6A

![]() ≈4.4M jobs

≈4.4M jobs

![]() $132,903 median income3

$132,903 median income3

Fill gaps in employer coverage to create opportunities in this high-income market with long earning horizons.

Sales Idea

Freelance Workers

Sales Idea

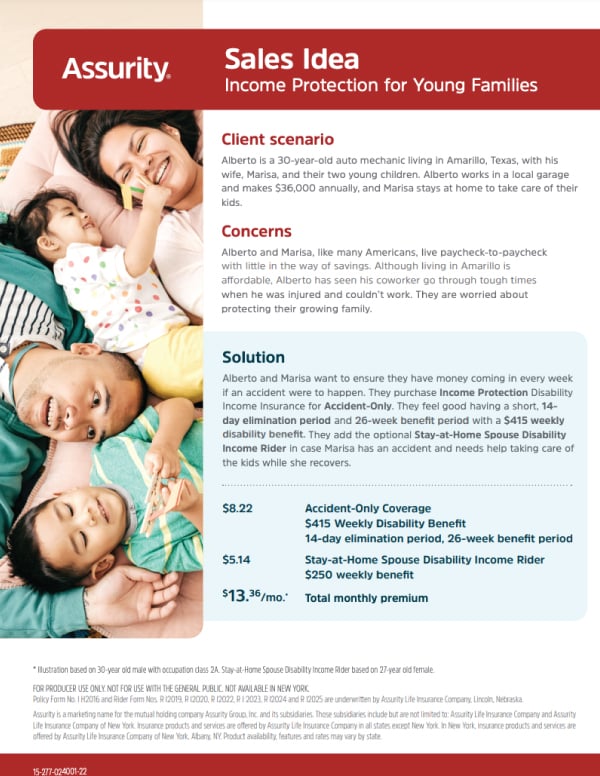

Young Families